This is the complete guide to Home Loans in Brisbane.

In today’s guide you’ll learn:

- How to find the best home loan in Brisbane

- How to choose between variable or fixed home loans.

- How to uncover hidden bank fees

- Which bank is the best for home loans

- Dozens of Home Loan Best Practices

In short: If you want to buy a home or refinance, and need a loan you’ll love this new guide.

- Chapter 1: Home Loan Basics

- Chapter 2: How to get the best home loan in Brisbane

- Chapter 3: How to choose between variable or fixed rates

- Chapter 4: Must have Home Loan Features

- Chapter 5: How to uncover hidden bank fees

- Chapter 6: Which bank is the best for home loans?

- Bonus chapter: Advanced Tips and Home Loan Best Practices

Chapter 1 Home Loan Basics

In this chapter I’ll cover Home Loan Basics.

(Including what the best features are and why they’re important)

So if you’re getting stated with finding a home loan, this chapter is for you.

Let’s jump right in.

Do You Have Enough Deposit?

If you don’t have enough deposit, looking at home loan options is pretty much impossible.

Why?

Because without a deposit, or the help of a guarantor you won’t be in a position to get a home loan.

(Most banks need 8-10% deposit these days)

You can find out if you have enough deposit using the Deposit Calculator.

Enter how much you have in savings, how much deposit you put down (8%) and the interest rate you expect.

And the calculator will let you know what your home loan options are.

What makes the Best Home Loan in Brisbane?

The best home loan is going to come down to your individual situation.

If you think you will be able to make extra repayments, and pay down the loan faster than a variable rate could be most suitable.

But if you’re looking for stability, or are concerned about interest rates going up a fixed interest rate might work.

Then there is type of loan to consider…

Why is the type of home loan important?

Some banks charge higher rates for investment loans, compared to home loans to buy a house to live in.

These day getting the best home loan comes down to one thing: repayment type.

In 2019 if you are buying a home to live in, almost every bank will need you to take Principal and Interest repayments.

(In other words, you are paying back the loan you borrowed from the bank as well addition to the interest)

So, if you are buying an investment property then its fine to look at interest only repayment… but these do often have a higher interest rate.

Why cheapest interest rate should be your #1 Goal

I should point something out:

The term “Cheapest Interest Rate” is completely misleading.

Yes, you want to have a cheap interest rate. But it should be your #1 goal.

Here’s why:

Let’s say you are a Police Officer, or Nurse that earns regular overtime.

And that overtime forms 5% of your total salary.

Well, if you applied for a loan with 2 of the big 4 banks that don’t accept overtime you could have your loan rejected!

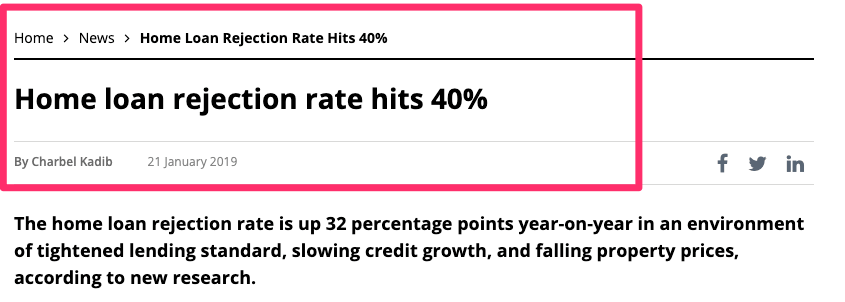

…Not to mention that recent industry figures show that mortgage rejection rates have risen from 8% to 40% of loan applications in 2019.

Put another way, 4 out of every 10 home loan applications are being declined right now.

Bottom line? Having a cheap interest rate is nice.

But the ultimate goal of getting the best home loan is just that, getting a home loan approved in the first place. 9 times out of 10, these two goals align. But it’t an important distinction to make.

With that, its time to dive into chapter 2.

Chapter 2 How to get the best home loan in Brisbane

This chapter is all about the critical first step of your home loan journey: Finding a loan.

And let me be clear about something:

Most people skip this step. And they end up going back to the bank they’ve always been with (Dollarmite anyone?), hat in hand hoping they’ll get the money.

Sure, you might get the bank manager on a good day.

But if you want to get 2-3x the amount of options, this initial research is KEY.

So without further ado, here’s how to CRUSH finding the best home loan in Brisbane.

Your Personal Goals

Your first steps are to set up goals for yourself and what you want to achieve with your home loan…

For example, let’s say you are a first home buyer.

Your goal might be to buy your first home in the next 3 months. Or save up a little more deposit to save on the lenders mortgage insurance.

Either way, it’s important to set those high-level goals BEFORE you get into the weeds of home loan products, features and policies.

The 5 most common home loan goals we see are:

First Home Owner wanting to stop renting, or living with parents and buy a home.

First Home Owner wanting to stop renting, or living with parents and buy a home.- Second home owner running out of space and wanting to upgrade your home.

- A First time investor wanting to buy an investment property, or grow a property portfolio.

- Home owner wanting to build a brand new home.

- A home owner or investor wanting to refinance their uncompetitive mortgage.

Which are you?

Once you’re clear on your high level goals its time to drill down a bit further.

That way, you can make sure you find a home loan that not only works for you, but can actually get the property you want…

Your Property Goals

So now you are clear on your personal goals, its time to set specific property goals.

And what I mean is getting specific on the type of property you are looking at buying, and a shortlist of suburbs.

Here’s why:

Because not all banks, like all properties or all loan purposes.

Building a Home

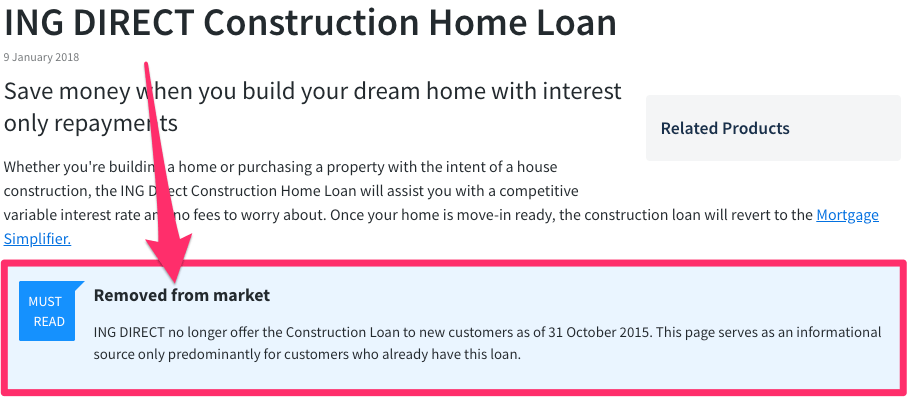

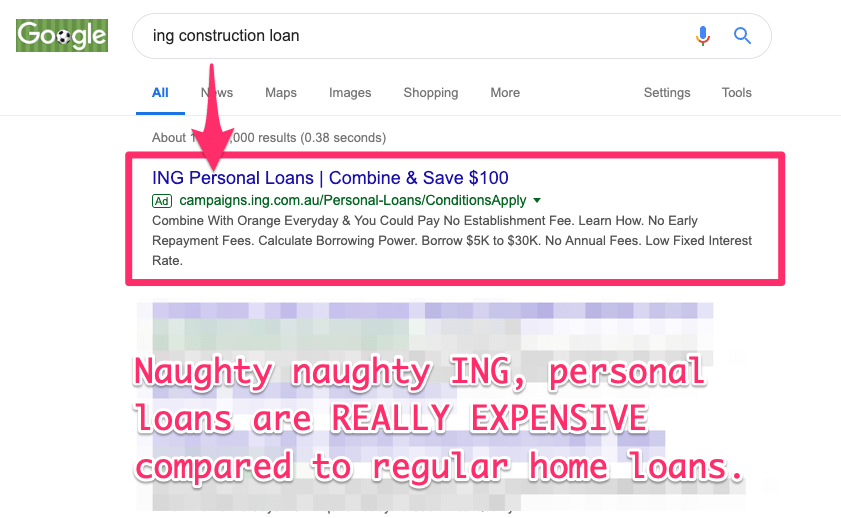

For example, there are banks like ING who do not do renovation, construction or building loans.

In other words: even if ING Direct had the best home loan product, they would decline your construction loan.

…Or worse, offer a personal loan and charge an interest rate TWICE the cost of a home loan.

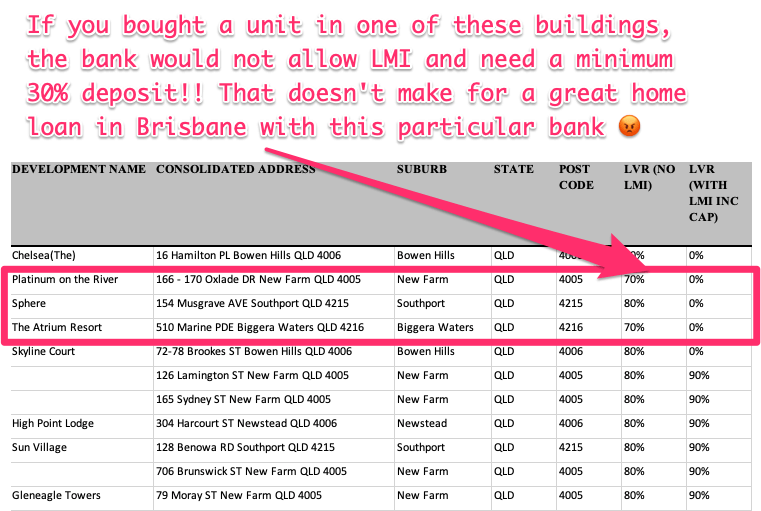

Buying a Unit or Apartment

Some banks won’t lend in particular post costs like Brisbane’s CBD because it is high density.

Other banks go one step further and will restrict lending if you are buying an apartment in a SPECIFIC building.

For example with one major bank buying in Sphere apartments would need a 30% deposit.

Buying a flood affected Property

…Or what happens if you buy a house that is in a flood affected suburb?

Did you know over 20% of Brisbane’s suburbs were flood affected in 2011?

Sure you can get lending, but you may need to pay for an engineering report to describe the type of flooding the property has experienced in the past.

As you can see having clarity over this stuff is critical to make sure you are aligned to lenders that can help with what YOU want to achieve.

(And not the other way around)

Your Short to Medium Term Goals

Now you know what you’re doing, and where you’re buying.

What will tie this all together back to finding the best home loan are your short to medium term goals.

You can decide on this by breaking it down into:

- Short Term Goals: 1 to 5 years

- Medium Term Goals: 6 to 15 years

There are a million different goals you can set, but try to keep them specific to your property and your loan.

In particular:

- Do you want to pay down your home loan faster?

- Are you looking to build wealth through property investing?

- Will you look to renovate your home?

- Or even upside to have enough room for a growing family?

Understanding these goals will help you decide between a fixed, or variable home loan.

Speaking of…

Chapter 3 How to choose between variable or fixed rates

In this chapter you’ll learn how to pick between variable or fixed rates like a pro.

So if you’ve ever asked yourself:

“Is a variable or a fixed rate better than me?”

“Should I use redraw or an offset account?”

“Is now a good time to fix?”

This chapter has you covered.

What to Compare First?

One of the biggest questions people have about choosing a loan is:

“What do I compare first?”

It’s a tough question to answer. After all: there are over 4,351 home loan products in Australia, and over 30 different banks and lenders.

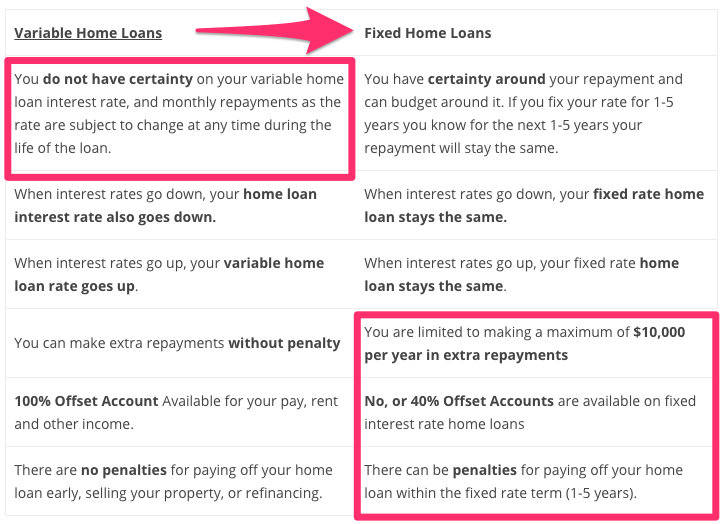

That said, here are 3 scenarios to help you decide on a fixed or variable home loan rate:

1. You are a person that likes stability, and the ability to budget.

You have read the barefoot investor, you have your splurge, smile and fire extinguisher accounts…

Or you like to know exactly how much your loan is going to cost you over the next 1, 2, 3 years.

While you’d like to make extra repayments on your loan over that time, its unlikely you are going to pay more than $5,000 to $10,000 in extra repayments per year.

You are wanting to settle into your new home, get comfortable with making your repayments and then look to make extra repayments in the future.

If this is you, then Fixed Rates are a great choice.

2. You are a person that wants to pay down your mortgage, or has the ability to make extra repayments each month.

You could have also read the Barefoot Investor, but found the Domino Your Debt chapter more interesting.

Or you get paid bonuses, or have a bit of a higher income and can afford to make more than the smallest loan repayment.

You might be looking to pay down your loan or cut years from the standard 30 year loan term.

And you might even have some cash left over that you want to offset the loan after you settle in, or redraw for the future.

If this is you, then Variable Rates might be a good choice.

Fixed and variable rates both have their advantages and disadvantages.

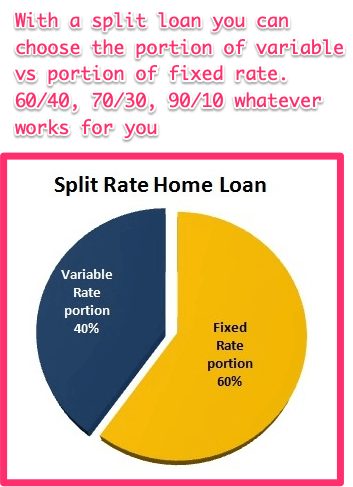

3. Porque no los dos!

Transaction: Why don’t we have both?

You might be thinking to yourself having a bit of stability, and the option to make extra repayments would suit you…

You might want to have some of your loan variable, and some of the loan as fixed.

If this is you, then a Split Loan could work well!

Create a Mock Mortgage

Now that you’ve decided which option is best for you, its time to create a Mock Mortgage.

In most cases, the banks will lend you MUCH MORE money than you usually want.

The best way to approach this is to work backwards from a weekly, fortnightly or monthly payment figure that you are comfortable with.

Put another way, if you are comfortable with paying $500 per week in mortgage repayments than why apply for a loan that will cost you $1,000 a week.

It will mean you’ll be on 2 Minute Noodles for the next 30 years!

Have a go at setting up your Mock Mortgage here.

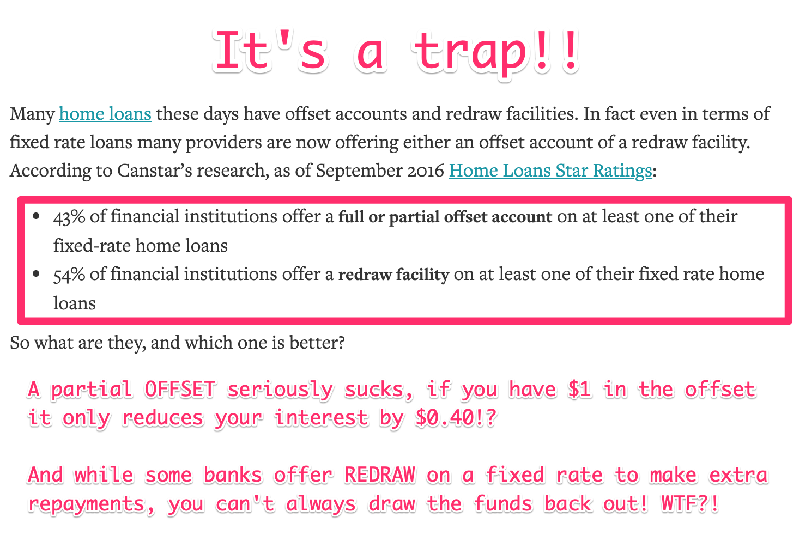

Battle Royale: Offset Account vs Redraw, which is better?

In short yes, a redraw facility has the same net benefit as an offset account being you can make extra loan repayments to reduce your interest payable – but also be able to draw the funds back out.

But there can be some confusion around the difference between an offset account and a redraw facility.

There are a few key differences that will help simplify the benefits of an offset account over a redraw facility.

The key differences include:

Offset account:

- Money is accessible at any time.

- Acts as a regular savings account and holds spare money.

Some transaction fees.

Some transaction fees.- Discipline is required as the money is so easily accessible.

Redraw facility:

- Enforced discipline as the money is not easily accessible – you need to apply for the money in advance.

- Usually has lower fees, and interest rates than loans with Offset Accounts

- Only available for additional repayments that go beyond your standard monthly repayments.

- Some banks charge fees if you are making more than 1-2 redraw withdrawals per month.

One word of warning: a partial offset account, against a fixed rate is a scam.

How to Know if Now is a Good Time to Fix?

Here are two tips to help you choose if now is a good time to fix:

First, don’t listen to the market.

I made the mistake of fixing my interest rates at a time when everyone in the media said rates were going up.

And they ended up dropping…

BY 4.25% in 9 MONTHS!!

Yeah that cost me $5,301 in break costs.

Bottom line: No-one knows which way the interest rates are going, so don’t fix because a media commentator said so.

Second, only you know if its a good time to fix for you.

At this stage you know your goals, the type of property you are looking at buying and your short to medium term plans.

If you’re looking for:

- Certainty of repayments

- Ability to budget

Then now could be the right time to fix for you.

If you’re thinking about:

- Making extra large repayments to your loan

- Selling your property within the fixed period

- Refinancing your home loan inside the fixed term

- Renovating or building a new home and want to use the equity during your fixed rate term

Then now might not be the best time to fix.

Chapter 4 Must have Home Loan Features

As you know, a bank will give you a home loan for 30 years.

But I don’t believe you should pay your loan off over 30 years.

Instead, the goal should be to cut 15 years off your loan.

And in this chapter you’ll learn how to cut years, and save thousands of dollars in interest.

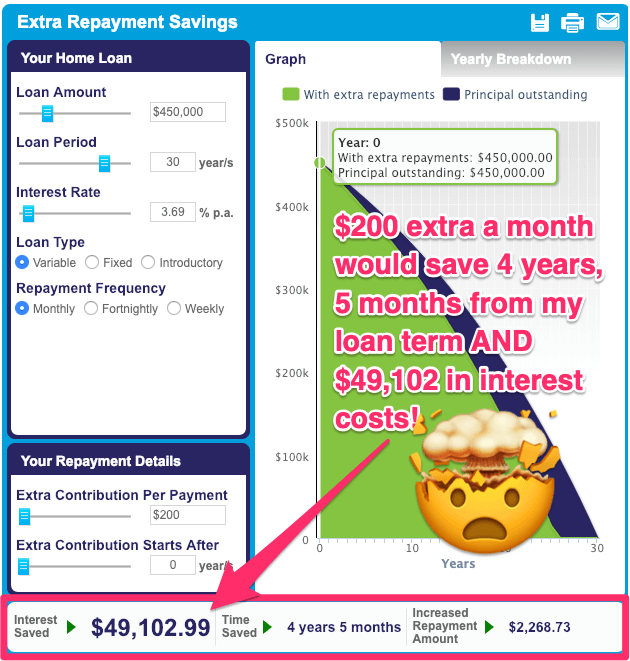

Cut Years From Your Loan With Extra Repayments

According to ASIC:

Anything extra you pay in the first 5 to 8 years (when most of your payments go towards paying off the interest) will cut your interest bill and shorten the life of your loan.

Don’t delay paying off your home loan if you can avoid it. Instead, try to make small regular extra repayments.

Here’s an example:

Try: Extra Repayment Calculator

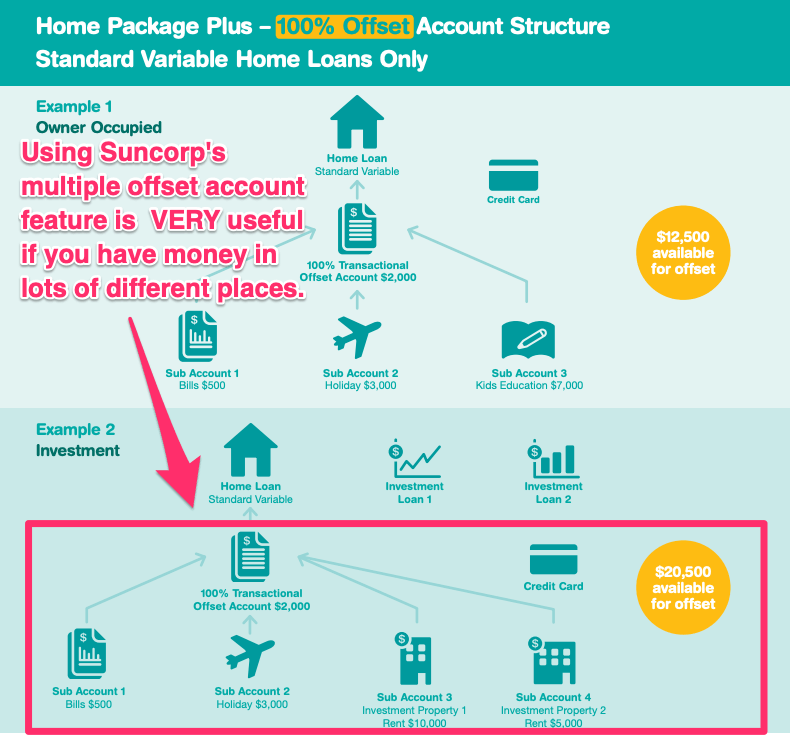

Multiple Offset Accounts

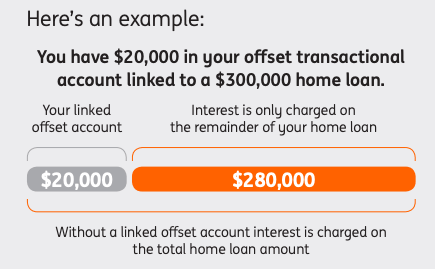

Offset accounts are like a normal transaction account, but instead of earning interest they save you interest on your home loan.

Makes sense, but what about having more than one offset account so every dollar you have reduces your interest costs.

Here’s a great example of multiple offset accounts in action:

See how this couple has got all of their different accounts working to reduce the interest on their home loan? Clever… and super effective.

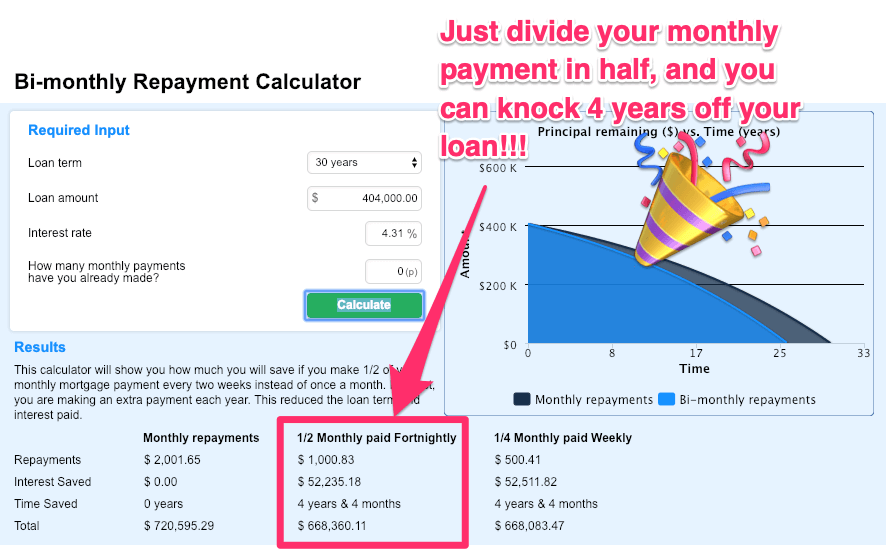

Increasing Your Repayment Frequency

Most banks, by default, give you monthly repayments…So in a year, they will assume you make 12 repayments.

Let’s say your monthly repayment is $2,000.

In a 12 month period you will make $2,000 x 12 months = $24,000 in repayments. Simple right?

If you switch to bi-monthly (also known as fortnightly) repayments, you will make an extra 2 repayments without even realising.

So you make $1,000 payment ($2,000 divided by 2) every fortnight which there are 26 per year = $26,000 per year in repayments!

You will make an extra $2,000 in repayments per year without even realising AND save 4 years and 4 months from your loan!!!

Read More: Pay Off Your 30 year Home Loan 6 Years Faster  [10 Easy Tips]

[10 Easy Tips]

When is the best time to start making additional repayments?

As you have seen from the examples above, the sooner you start making additional repayments the faster you will pay off your home loan.

Home Loan Extra Repayment Calculator

Chapter 5 How to uncover hidden bank fees

If you have a bank account, you already know that banks loooovveee charging fees.

The question is:

How do you find out about these fees before you sign up to your new home loan provider?

That’s exactly what this chapter is all about.

It’s a collection of 4 techniques specifically designed to help you uncover every hidden fee and sneaky charge banks will hit you with.

Ask for a Lenders Mortgage Insurance Comparison

Lenders Mortgage Insurance (or LMI) can costs anywhere from a few thousand up to TENS OF THOUSANDS of dollars.

I’ve personally paid over $50,000 in LMI across the various properties I’ve bought over the years.

And while it isn’t cheap, it is often a necessary cost to get into a property faster.

BUT just because you have to pay LMI, doesn’t mean you need to pay top dollar.

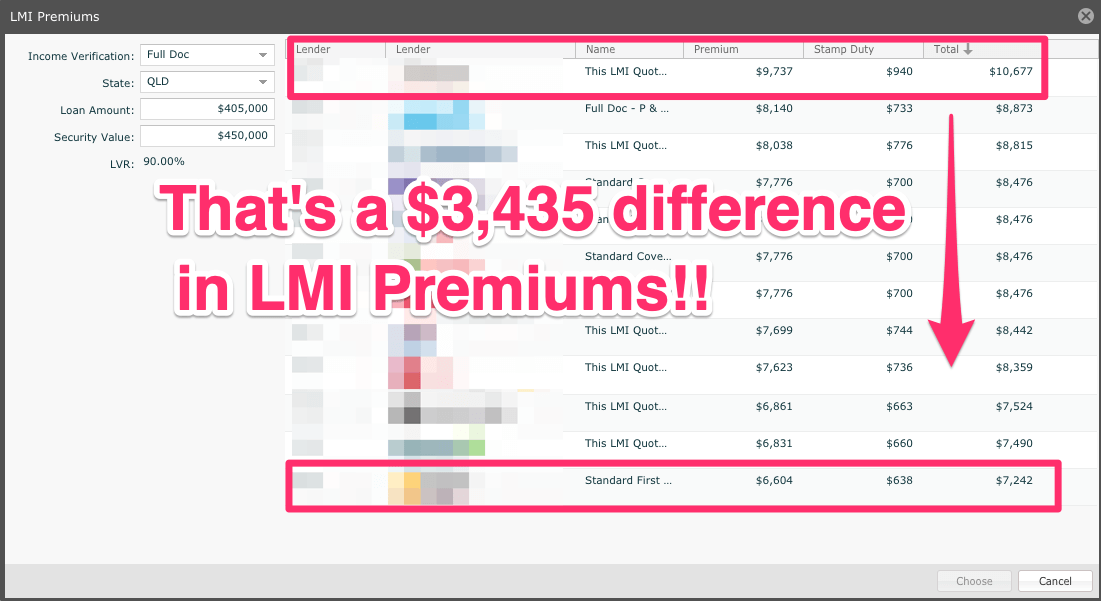

How to Get the Best LMI Deal?

There are some mortgage brokers who only take into account the interest loan charged by various lenders.

But if you want to get the whole financial picture, it is very important to keep every loan feature in mind.

In this situation, there is a $3,435 different in LMI costs between banks!

If you wish to find the best deal, there are three things you should keep in mind

- Find out the LMI providers, lenders, and discount you qualify for

- Specify what you need, why you applied for a loan, and what particular features you want in your loan

- Compare the packages offered by different lenders, including the LMI premium, fees, interest rate, and other loan features.

Following this three-step approach will definitely help you secure a good deal and it is possible to do so with an LMI calculator.

Get ALL details of Exit Fees, Settlement Fees, Discharge Fees, Ongoing Fees and Application Fees

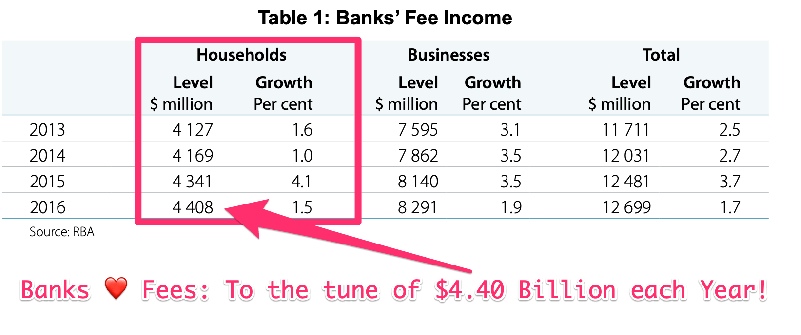

According to the RBA, the bank make over $4.04 BILLION (yes, billion) in fees each year.

That’s a lot of fees!

The most common fees include:

FeeAmountWhatNegotiable?Exit FeeNilThese were banned a few year ago and do not apply to regular home loans.N/ASettlement Fee$0-$200Banks will charge a settlement fee to arrange settlement and cut cheques for your home loan.Sometimes, depending on bank.Discharge Fee$300-$350When you either sell your home, or refinance your bank will charge a fee to arrange the discharge of your mortgage.NoApplication Fee$0-$600If you are not applying for a loan on a Professional Package, or a Basic Home Loan which has no ongoing fees the bank will sometimes charge an application fee.Sometimes, depending on bank.For example St George have a promotion where they are giving a $1,000 rebate for First Home Buyers.Ongoing Fees$0-$395If you are applying for a loan with a Professional Package, it often has an annual fee which waives the monthly costs of your credit card, offset account and any future loan variations.Sometimes can get the first year waived.For example Suncorp have a promotion where they will waive the annual package fee for first home buyers.Valuation Fees$0-$200Most banks will include one free valuation as a part of your application but if you have more than one property you may be charged for additional valuations.Usually free for first property, sometimes negotiable if you have 2 or more properties.For example, some of the major banks have refinance rebates up to $2,000 at the moment which will help cover the costs of valuation fees.They’re the most typical fees, some like LMI are unavoidable without having more money in deposit but its still worth knowing.

Chapter 6 Which bank is the best for home loans?

There’s no other way to say it:

Your Home Loan Application can make or break your home ownership journey.

Use the wrong bank?

You may as well say: “Farewell home”

But when you use the right Bank, with the right home loan you’ll find an easy and simple home buying process.

So without further ado, here are simple (yet effective) strategies you can do to get into your home quickly and easily.

Get All Of Your Information Through

Want to make sure you can qualify for a loan… without any nasty surprises? Try providing all of your information upfront.

Here’s why: You might be on $56,000 annual salary, but your work might do salary packaging or you could have been on holidays recently.

Or could have a HELP debt, or are paid $56,000 including super…

Any of these changes could drastically change your borrowing capacity, so if you are spit balling how much income you are on vs. getting your broker to verify from your payslips it can make a world of difference.

Ask What Type Of Pre-Approval Your Bank Provides

Not all banks are the same when it comes to assessing a pre-approval home loan, also known as a conditional approval, indicative approval, approval in principle or home seeker depending on the bank you use.

In most cases a pre-approval is just an indication that the bank is ok to consider approving your loan, they may just complete a credit check and not check any of or your documents and wait until you lodge a full mortgage application to do this.

A full mortgage application is done when you find a property and means the lenders will complete the entire assessment of your loan, they will verify your payslips, bank statements, your income information, savings information and any liabilities you have to be 100% sure they can lend you the money.

Unfortunately, if you have gone out and got a pre-approval from a bank the lender is under no obligation to then fully approve your loan once you have found a property. They can say your situation has changed and knock you back.

Which Lenders Provide Unreliable Pre-Approvals?

Be cautious of any system generated approvals from St George Bank, Westpac Bank, Suncorp, ANZ, NAB or any other bank that gives an on the spot pre-approvals.

If you have a NAB pre approval, or ANZ pre approval you should make sure to ask the questions above to confirm it is a real approval. If you aren’t sure, get in touch with our team, call us on 1300 088 065 or get in touch online so we can review for you.

At Hunter Galloway we work with lenders that will verify your income and deposit information to ensure you have a verified pre approval.

In the case of many of these banks while they may complete a credit check, and provide approval in principle your application hasn’t been assessed from the credit department and therefore the bank could change their decision to lend you the money at a later date.

Read More: What is Pre Approval? Ultimate Guide

Bonus chapter Advanced Tips and Home Loan Best Practices

Now that we’ve covered the basics, its time to go advanced.

In this chapter, you’ll see advanced tips and Home Loan best practices that you can use to get the best home loan in Brisbane… FAST

Close Out Your Unused Credit Cards & AfterPay

Each time you apply for AfterPay, ZipPay or a Credit Card the lender will leave a credit check.

And more than 3 credit checks in a year will significantly reduce your credit score.

(To the point where some banks will straight up decline your home loan application)

It is possible to increase your credit score, according to ASIC you can do this by:

- lowering your credit card limits

- consolidating multiple personal loans and/or credit cards

- limiting your applications for credit

- making your repayments on time

- paying your rent and bills on time

- paying your mortgage and other loans on time

- paying your credit card off in full each month

Credit scores help lenders decide if they should lend money to you. Knowing your credit score can help you to negotiate a better deal with your bank or find an alternative lender that will reward your good credit history.

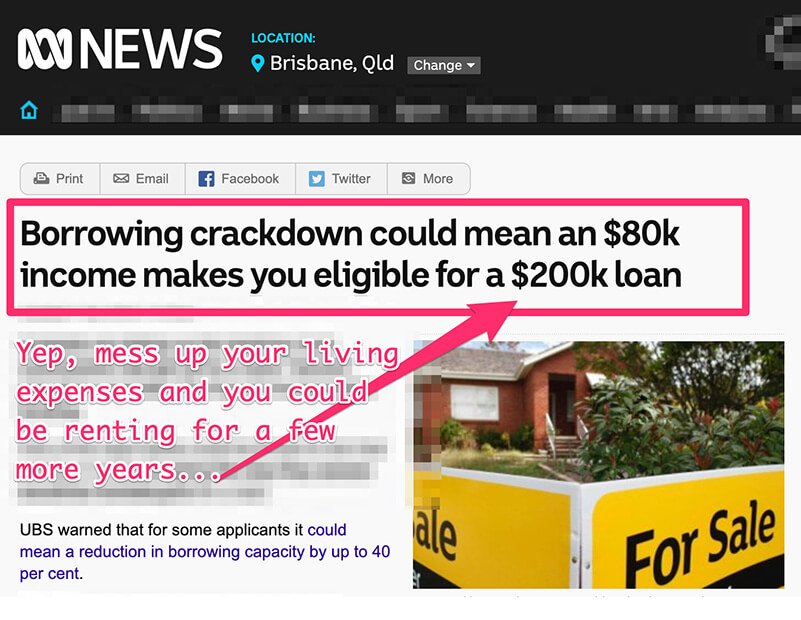

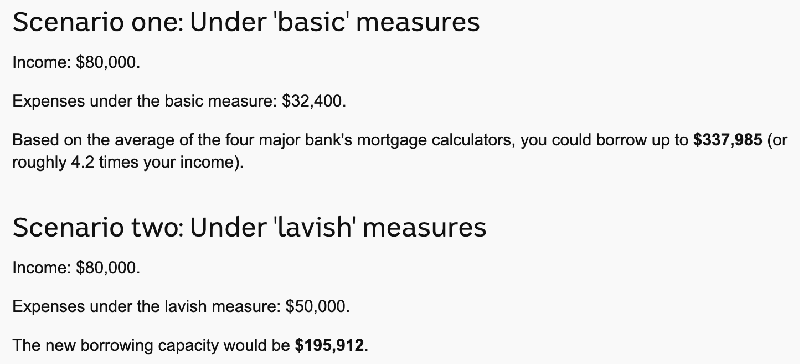

Clean Up Your Living Expenses

These days, a bank will flat out decline your home loan if you spend too much each month on Uber Eats, Dan Murphys, Netflix or Sportsbet.

For example, last year Westpac changed its living expense credit policies increasing the number of living expense categories from 6 to 13, to get home loan applicants to provide WAYYYY more detail about what they spend their money on.

Once they have that information you’ll be put into one of three lifestyle categories:

Basic

Basic- Moderate

- Lavish.

And this can make a massive difference to how much the banks will lend you.

Yup, legit check this out:

If you’re living too lavish, you can only access just under half the borrowing amount as if you live a basic lifestyle.

This is part of what your Mortgage Broker will review with you, but between 3-4 months before you apply for your home loan make sure you’re not having any Dan-Murphys-benders or going too hard on the multis.

Find out What Documents They Will Need

Some banks need a few documents, other banks will want A LOT of documents.

(They are lending you hundreds of thousands of dollars so it only makes sense for them to ask for a bit of information)

Question is, do you have all the info the bank is going to ask for?

Most common documents include:

- Your 2 most recent payslips

- The most recent years PAYG Payment Summary, also known as a group certificate

- Last 3 months day to day transaction account statements (where you are paid)

- Most recent months statements for any open credit card, personal loans, or AfterPay accounts

Have these documents ready to go before you start talking to your Mortgage Broker.

…It’ll speed things up heaps

See If You’re Entitles to Any Perks with Your job

Do you know the banks have a secret list of jobs that qualify for waived lenders mortgage insurance?

Put another way, if you work in one of the following jobs you can buy a home with a 10% deposit (and in some case 0% deposit) and not have to pay any LMI.

SAVING YOU THOUSANDS

Instead of paying monthly for a rental, Australians are looking towards buying, as it allows them to take one step at a time toward owning a property. More and more working professionals are applying for home loans, including:

- Medical doctors (who can qualify for up to 100% no LMI)

- Accountants

- Dental surgeons

- Chiropractor

- Veterinarian

- Pharmacist

- Optometrist

- Entertainment professionals

- Professional athletes

- Lawyer

Read More: Awesome! No LMI

Now it’s your turn

I hope you enjoyed my guide to Home Loans in Brisbane.

Now I want to turn it over to you: Which of these tips from today’s guide are you going to try first?

Are you going to try making bi-monthly payments? Or start comparing LMI fees?

Let me know by leaving a quick comment below right now.